Brasil - always the country of the future. "Brasil is the country of the future, and always will be"

Brasil is a large country, ranked sixth in the world by land mass (8.4 million square kilometres, Aust ranks 7th at 7.7m), ranked 6th by population (210m - almost 10 times the size of Australia), with a GDP ranked 9th largest in the world at US$1.869 trillion (Australia ranks 13th with a GDP of US$1.4 trillion). However, this top 5 economy by population and top 10 economy by land area and GDP ranks 97th by GDP per capita, and is a developing (not developed or advanced economy) with a GDP per capita of just over US$8,820 compared to Australia's rank of 13th and GDP per capita of US$57,000.

The low level of economic development is accompanied with low levels of productivity, low levels of international competiveness, high levels of corruption (ranked 106th amongst 180 nations for transparency) and high levels of income inequality. Of 158 countries measured by the World Bank, with a gini co-efficient of income inequality of .569 Brasil ranks as the ninth most unequal income distribution on earth, behind mostly African nations.

Unlike developing economies in sub Saharan Africa, Brazil is blessed with very significant endowments of natural resources, especially in relation to agriculture and minerals. Brazil is a major global economy in terms of mining, agriculture, and manufacturing, and has a strong and rapidly growing service sector. Significant mineral resources include iron ore, tin, bauxite (the ore of aluminum), manganese, gold, quartz, and diamonds. It is a significant global exporter (25th in the world despite being the world's 9th largest economy), exporting significant volumes of iron ore, steel, automobiles, electronics, and consumer goods. Brazil is the world’s primary source of coffee and oranges, and a major producer of sugar, soy, and beef. Brasil has a very narrow export base, with 3 commodities (iron ore, soy beans and oil) accounting for more than one third of total exports - making Brasil trade balance (Current account) quote volatile responding to commodity price and currency movements.

The key to understanding the Brazilian economy

Brasil is a massive economy which only emerged into democracy from a harsh military dictatorship in 1985. Many of the protestors and fighters against the military dictatorship, including subsequent Presidents Lula and Rouseff, were in fact fighters against that regime, suffered torture, and formed the left aligned Workers Party (the PT). Even before the military dicatatorship, Brasil had a statist interventionist approach to management of the economy. This can be seen in the pursuit of the Import Substitution Industralisation developmentalist approach which delivered strong growth for a period, however proved unsustainable in the face of external inflationary and interest rate shocks leading to hyperfinflation. Through stablisation plans, including a new currency (eventually floated) and implementaiton of more conventional macroeconomic frameworks (the macroeconoic tripod of inflation targetting, floating currency and fiscal targets), Brazil stabilised the economy before riding the commodities super cycle caused by the industrialisation of China punctuated by the GFC. What hyperinflation looks like - Venezuela

That supercycle provided the government with increased revenues,and coupled with resource discoveries, Brazil enjoyed high rates of economic growth and were clustered with key emerging economies into the grouping of the BRICS, alongside Russia, India, China, and then joined by South Africa. The supercycle also coincided with the election of PT President Lula (on the fourth attempt) which meant that the supercycle was used as a platform to increase government spending with a view to lift Brazilians out of absolute poverty through a range of social programs (Bolsa Familia, Fome Zero), and then a series of large scale infrastructure programs (growth acceleration programs styled PAC1, PAC2). However, significant micro reforms in relation to the labour market, pensions, cost of doing business, and corruption were not addressed - such that the growth masked the underlying structural weaknesses of the economy, and the structural weakness of the fiscal position. Subsequently under Presidents Temer and Bolsanaro there has been a start on micro reforms including pensions.

With stronger macro frameworks in place in relation to primary fiscal surplus targets (Fiscal Responsibility Law 2000) and an independent central bank conducting inflation targetting monetary policy via the SELIC rate, Brasil was able to weather the GFC with similar policy responses to Australia - loosening fiscal policy and expansionary fiscal policy. Brasil was one of the first economies to recover from the GFC, recording very strong GDP growth of 7.5%.

Unlike Australia, the commodities supercycle did not launch business investment as the driver of growth in the economy. For Brasil, where consumer spending represents over 60% of GDP, growth was being driven by increased incomes, household consumption (often fuelled by government transfer payments and cheap credit being provided by state owned banks) and population growth. When commodities prices softened, President Rouseff (the PT successor to Lula who by law could only serve 2 consecutive terms) turned interventionist in relation to the economy in an attempt to control inflation (worsened by depreciation of the currency) by regulating a range of prices in the economy for utilities, transportation and food, and interefered with monetary policy directing the central bank to lower interest rates to increase growth even though inflation was outside the band. This was accompanied by expansionary fiscal policy - even though the Brasil budget had been in deficit throughout the entire period of the commodities supercycle, and was outside parameters in terms of a primary fiscal surplus.

The result of the government intervention was a loss of domestic and international investor confidence, a reduction in growth, an increase in unemployment, continuing depreciation of the real and stagflation. Eventually monetary policy returned to its independent inflation targetting role, and was increased throughout to control inflation which is now at historic lows and interest rates have been reduced. From a fiscal perspective, the budget deficit has reduced, although is still 7% GDP and government debt has increased to more than 77% of GDP.

With a significantly weakened economy as the growth drivers of subsidised household credit, population growth and high commodity prices abated, and with the policy levers of monetary and fiscal policy being used to reduce inflation and the budget deficit, the economy was significanlty impacted by the world's largest ever corruption scandal - Operation Car Wash, which involved a number of Brazil's largest companies, a large number of politicians and business people. Petrobras, the largest company in Brasil, and the world's fourth largest company, was involved in massive corruption in connection with the construction of investment projects and the investigation led to the stalling of projects, reducing business investment and directly increasing unemployment - worsening the crisis.

Brasil then entered its worst economic crisis since 1900.

Significantly, this crisis occurred because of the failure to undertake micro reform (including addressing corruption), and to use the positive influence from the global economy with the commodities supercycle and cheap credit to undertake social reform without undertaking fiscal and micro reform, and then the short lived, unsuccesful return to state intervention which worsened the crisis by further negatively impacting global investor sentiment. Indeed, even where the government sought to encourage private investment in infrastructure and concessions, the terms on which the projects were offered (including state majority ownership) often resulted in no bidders for the concessions.

In turn, this is currently somewhat compounded by the appreciation of the USD as a result of the interest rate tightening by the Fed in response to the growth in the US economy and the countinuing, pro cyclical fiscal stimulus of the Trump administration. In other words external events also negatively impacted Brasil through changes in exchange rates - although arguably not as much as would have occurred if the degree of integration with the world was higher.

In 2017 President Rouseff was impeached (by the votes of members of Congress many of whom faced personal corruption charges) in relation to budget irregularities (not as a result of personal corruption), although her prior role as Chair Woman of Petrobras and the scale of corruption charges from the Car Wash investigation and the agitation by a closely held press dominated by wealthy families saw millions protest on the streets for her impeachment. She was replaced by Michael Temer - whom wikileaks identified in cables as a past CIA informant.

In the 2018 election Jair Bolsanaro was elected President effective 1 January 2019, and whilst a divisive figure, has pursued a pro business agenda and achieved long awaited pension reforms which will have positive impacts on sustainable fiscal policy in Brasil.

Specifics - ISI

Import Substitution Industrialisation is a development strategy where an economy borrows money from foreigners (increasing NFD, typically in foreign currencies) and uses the funds to develop domestic industries which are protected from competition by significant protection policies. In this way, imports are replaced by domestically produced goods (including steel, automobiles and aviation).

Import substitution was the main strategy used in Brasil in the 1950s to 1960s, and was in place from the 1930s through import licensing, tariffs, quotas, import prohibitions, overvalued exchange rates, and direct government investment in key industries. Tariffs were very significant, with automobiles 308%, textiles 123%, rubber 122%, vegetables 122% and clothing 117%.

With the availability of cheap credit from petrodollars in the 1970s, government and the private sector borrowed heavily generating high but unsustainable economic growth in the 1970s and 1980s. When oil prices increased both in 1974 and in 1979 and interest rates rose in 1980, the high accumulated debts (NFD) proved unsustainable, resulting in a debt crisis and a foreign exchange crisis. The result was almost 15 years of low growth and hyperinflation.

In this way, the ISI strategy, as a response to globlalisation, which was engaging with NFD but not NFE, maintaining high barriers to protection and extensive business operations by government was not a sustainable strategy as it was exposed to the downside fluctuations of global oil prices and interest rates.

By 1990 the ISI strategy resulted in Brazil having less than a 1 percent share in global trade, despite representing 3% of the world's population. From 1988, the government began a new policy of export promotion with the intention of inducing, through external competition, a more efficient allocation of resources.

The reduction in tariffs proceeded in stages, with a reduction in effective tariff rates from 68% to 39% (1987-1989), and the average tariff rate declining to 37% in 1990 to 15% by 1993. Brasil tariffs - world bank

Import substitution industrialisation - Britannica

Specifics - The Real Plan

In the early 1990s, at the end of the ISI approach, the economy was suffering having shrunk 3 out of the previous 6 years, and inflation being above 100% since 1982 reaching 2,500% in 1993. This led to a stabiisation plan referred to as the Real Plan.

The aim was to de-index the Brazilian economy - the situation where wages were previously automatically indexed for price increases which resulted in wage price inflation. Elements of wages became indexed to US dollars, which avoided foreign exchange related wage adjustments. Stabilisation of the economy led to the resumption of large scale capital flows to Brasil, and a resumption of growth.

The plan included a new currency (the real) pegged to the U.S. dollar, a more restrictive monetary policy, and a severe fiscal adjustment that included a 9% reduction in federal spending and an across-the-board tax increase of 5%. Prices immediately began to stabilize, with annual inflation falling from 2,730% in 1993 to about 18% in 1995.

In addition, a number of state owned businesses were privatised and a gradual opening of the Brazilian economy to foreign trade and investment.

However, the 1997 Asian Financial Crisis and 1988 Russian Financial crisis caused concerns about Brazil's exchange rate and budget deficit level which sparked massive capital flight leading the government to float the Real - at which time it lost 40% of its value.

Following the 1988-99 financial crises, the government adopted the three main pillars of its macroeconomic policy (also referred to as the macro tripod):

- a floating exchange rate

- a primary fiscal surplus (surplus before accounting for interest costs on government debt)

- independent monetary policy targetting inflation

In 2000 Brasil implemented the Fiscal Responsibility Law, a limit on budget spending in all levels of government. The Fiscal Responsibility Law sets a general framework for budgetary planning, execution, and reporting for the three levels of government which constrains public indebtedness and sets rules for general targets and limits for selected fiscal indicators, corrective institutional mechanisms in case of noncompliance and institutional sanctions for noncompliance. It also includes targets for primary fiscal surpluses, which were first introduced during the Russian crisis. Targets were 3.75% of GDP agreed with the IMF, later increased by Lula to 4.25% GDP. Note, however, that after interest payments Brasil continued to have budget deficits, and an increase in nominal government debt. A primary fiscal surplus does not mean a fiscal surplus - it means a surplus before interest payments on government debt.

The Real Plan successfully reduced inflation from hyperinflation levels to 20% per year within a short period of time, however was forced to subsequently float the Real, and adopt the elements of a more mature macroeconomic framework for the economy. On the other hand, since launching the Real Plan in 1994, only in the first 2 years following the Plan did Brazil's economic growth exceed the world average - and it grew below world average from 1996-2005.

Specifics - Lula and economic development

Luis Inacio Lula da Silva (known as Lula was elected President on the fourth attempt in 2002 as the leader of the Workers Party (PT) which he founded as a metal worker and union leader. Whilst markets were concerned about leftist economic policy, in government he maintained the market oriented reforms of prior government, and raised the level of the primary budget surplus

Lula controlled expenditures, raised the primary budget surplus to 4.25%, and granted additional independence to the Central Bank. However, his key contribution was in relation to reducing poverty, reorganizing and expanding existing social. The most high-profile program, Bolsa Familia (“Family Grant”), provides monthly cash payments to poor families that ensure their children attend school and receive proper medical care. This is referred to as a conditional transfer payment. During his second term Lula established a larger role for the Brazilian state in economic development. He expanded Bolsa Familia and launched new social welfare programs. He continued to raise the minimum wage, which increased nearly 64% in real terms during his eight years in office.

In response to the GFC, Lula implemented a series of stimulus measures (fiscal and monetary policy) designed to offset declines in global demand with increased domestic consumption. The crisis was addressed without changing the fundamentals of the macro tripod, which survived the crisis unlike the policy implications of previous crises.

Whilst GDP contracted 0.2% in 2009, strong growth in 2010 as 7.5%. With new, significant oil discoveries, Lula negotiated a a new regulatory framework that increased the state’s role in the new offshore oil reserves, and established a fund to use those resources to provide improvement in long term economic and social development.

On the other hand, given the growth impetus of the commodities super cycle, moderated by the GFC, and the abundance of foreign debt associated with low interest rates, Brasil's high growth, and resource discoveries critics identify the lack of significant micro reform in this period to improve the productivity of the labour market, industry and reforms to bloated public sector pension schemes. Between 2001 and 2011 the proportion of the population living in poverty fell from 37.5% to 20.9%, and the percentage living in extreme poverty fell from 13.2% to 6.1%, and income inequality was also reduced (Gini coefficient 0.64 to 0.56). According to a 2012 study, about 28% of the decline in income inequality in Brazil between 2001 and 2009 was attributable to increases in the minimum wage, and another 13% of the decline was attributable to the Bolsa Família program (with the balance from the terms of trade improvement.

Specifics - Rouseff and the interventionist swing

President Dilma Rousseff (PT) was Lula's appointed successor as Lula could not constitutionally stand for a third term. When standing down his approval rating was over 80%. Rouseff was elected in 2010, and again in 2015.

Rouseff promised to maintain the popular socioeconomic policies of Lula, however her first term included passing the peak of the commodities supercycle, declining oil prices, and pressures on Brasil's economic growth. This led to massive popular unrest, including mass demonstrations in June 2013, during which more than 1 million marched in the streets frustrated with the stagnation in their living standards, seeking better quality public services, and reduction in corruption. Whilst economic growth from 2002-2010 averaged over 4%, increasing employment, wages and living standards, a slowing China, increased iron ore supply and lower commodity prices resulted in the slowing of economic growth.

To support growth, Rousseff switched away from the macro tripod to a more state intevention, micro managing model of the economy. This was responding to globalisation with interventionist counter cycle government policy.

In practice, the intervention included measures to stimulate domestic consumption and protect domestic industries - a series of short-term tax cuts and subsidized credit through state banks.

Whilst successful in the short term, inflation increased to and beyond the band, and the budget deficit worsened as a result of the tax cuts. Rouseff directed the central bank to cut interest rates to encourage growth even with inflation beyond the band. Further intervention occurred in product markets, with price fixing in fuel and electricity prices, damaging the revenue and share price of government owned Petrobras. The intervention switch concerned foreign investors, resulting in further depreciation of the Real, capital repatriation, and a reduction in FDI flows.

Economic growth fell from 3.9% in 2011 to 0.1% in 2014.

The short lived intervention switch was reversed following election to a second term, concerned about bond ratings, currency levels, FDI flows and the deteriorating fiscal position. Rouseff implemented a range of austerity measures to stabilize debt levels, encourage investment, and boost growth in the long term. These measures included partial budget freezes, reductions in the number and size of government ministries, restrictions on certain pension and unemployment benefits, and reversals of several of the tax cuts granted during her first term, and allowing fuel and electricity prices to rise (worsening inflation). The central bank resumed independent inflation targetting, which was contractionary in terms of growth.

Unsurprisingly given the austerity measures and tightening cycle of monetary policy, economic growth was only 0.51% in 2014, with the economy signficantly shrinking in 2015 (-3.6%) and 2016 (-3.5%) before increasing in 2017 (1%). Much of the GDP and GDP per capita gains of the commodity supercycle and consumption driven boom had been lost in another lost decade for Brasil.

2014 also saw the opening of Operation Car Wash, a wide ranging corruption investigation which entangled Petrobras and a number of large construction companies, the result of which stalled major infrastructure projects and investments, negatively impacting economic growth at a time where growth was already fragile or negative. It was estimated to have wiped 0.75% off Brasil's GDP in 2015. Refer the videos on this corruption investigation in the resources section

Rouseff was impeached in 2016 for budget irregularities (not personal corruption). She was charged with “fiscal pedaling” for allegedly violating Brasil's Fiscal Responsibility Law by postponing required payments to state banks to compensate for budget shortfalls and thereby presenting a stronger (and artificial) fiscal position during her election campaign.

Specifics - Temer and austerity

Michel Temer is a 75 year old law professor who became the unelected President of Brazil following the impeachment of Rouseff in 2016. CNN 5 things to know about Brazil's interim leader

Despite personal implications in corruption, Temer survived votes in Congress to pursue corruption charges despite taped conversations suggesting such. In 2016 Temer secured congressional approval for a 20 year constitutional freeze on increases in inflation adjusted public spending. What this means is that for the next 20 years, growth in government spending cannot exceed the annual inflation rate in the Brazlian economy. It follows that if economic growth exceeds inflation, then then spending as a percentage of GDP will decline (over the medium to long term) and the budget deficit will decline as a percentage of GDP. This is important to reduce the growth rate in government debt, which has risen to 80% GDP.

However, to achieve the spending cap will require social security reform (since achieved by Bolsanaro) - indeed some 40% of the Federal government's primary spending (before interest payments) is consumed by social system benefits - much of which does not go to the poorest but to middle and upper classes in the form of government pensions for early retirement age public officials. Social security system benefits have been growing at least 4% in real terms (which would need to reduce to 0% in real terms under the cap).

In Brasil, retirement can occur after 30 working years for women, and 35 years for men, with Brasil's spending as a percentage of GDP similar to OECD nations, and is more generous - paying 80% of pre retirement income compared to OECD averages of 60%.However, despite attempting reforms of the pension system directed towards lower benefits, higher retirement ages, and less skewing of benefits to the public sector, Temer was unable to achieve those reforms prior to the 2018 election which he did not contest as his approval rating was around 5%. Reform was subsequently achieved by Bolsonaro.

However, during Temer's period independent monetary policy remained in place, budget deficits were slightly reduced although still at concerning levels, and moves towards privitations with a $14b drive including the sale of Electrobras and 56 other public companies, airport terminals, electric transmisson lines, port terminals, two highways and the Brazil mint. Of course, whether privitisations proceed will depend on the economic policy stance of the incoming President, a right wing candidate.

Lazard Asset Management provides excellent summary of Temer reforms and future challenges

Specifics - Bolsonaro - Trump of the Tropics

Jair Bolsonaro is perhaps even more Trump than Trump in terms of his extremist conservative views (Bolsoaro's worst quotes, however from an economic perspective is pro business, pro development, and pro US. Despite his attitudes and extremist positions, he did oversee the achievement of very significant pension reform with attendant positive impacts on Brasil's medium term fiscal position. The changes to the pension arranagements, which required constitutional changes are estimated to result in savings of US$195 billion over 10 years. The rate of privitisations also stepped up, with $23 billion of asset sales in 2019, independent monetary policy preserved (with the lowest SELIC rate ever in response to low inflation and low growth).

On trade policy, Bolsonaro was able to avoid US threatened tariffs on steel, but Brasil remains exposed to unilateral protection increases by the US. Bolsanro shares Trumps disdain for multilateralism, globalisation and free trade - although US actions in that regard may be contrary to Brasil's interests threatening exports, AD and economic growth in Brasil.

Corruption remains a major issue, and a policy faillure in not addressing. Both of Bolsanaro's two eldest sons are being investigated for corruption.

On the environmental front, Bolsanaro is an active supporter of unhindered development of the Amazon and significant weakening of environmental laws and protections - including weaking the domestic environmental protection authority by cutting its budget. In 2019 Amazon fires increased by 84% in one year which results both from natural causes in lightning strikes, but also as a result of deliberately lit fires to illegally deforest lange in order to enable expanded cattle grazing operations. The scale is immense, with 74,000 fires detected in 8 months. This is still a lower level than 2010 - but the reduction was a result of increased environmental protections which are now being removed. Amazon fires.

Bolsonaro's first year: Balancing the economy and cultural wars | Sumary of economic policies

Specifics - The challenges

Brazil's continuing economic challenges, in order to take advantage of globalisation and moderate the negative impacts of external shocks, include:

- fiscal reform: further controlling spending as tax increases are not feasible as tax levels are already high in world terms. The most significant and urgent part of this is pension reform and social transfers which are largest to the highest quintiles. See Robin Hood in reverse: the crisis in the Brazilian state

- labour market reform: lower costs for travel time to work, reduced dismissal protection and greater support for casualisation of the work force

- tax reform: significant simplification is required - currently takes on average a company 2,000 hours to prepare tax returns, versus OECD average of 163 hours

- business investment: business investment levels are low in world times, and household consumption too high. An increase in business investment and capital deepening is required to increase productivity and increase international competitiveness

- imported inflation: US Fed tightening cycle will depreciate the Real, increase inflationary pressures, and may require higher interest rates to control inflation, although may provide support for export industries

- extent of integration with the global economy: increasing the global focus of domestic businesses, increasing international competiveness and increasing exports as a percentage of GDP

- corruption: the continuing car wash investigation continues to suppress and depress construction and investment in the oil and gas sector, and infrastructure construction, and may make political discourse more difficult to proceed with challenging austerity measures and micro reforms necessary to increase productivity and the sustainability of the fiscal position

Productivity problems and how to fix the economy now

- OECD labour productivity in brasil

- Accenture Accenture - Brasil's productivity growth

- How to fix the brasilian economy

- Reinventing Brasil - special FT liftout newspaper 2017

- Brasil US Business Council publication 2016

- Excellent emerging economy note update from 2017 from Lazard Asset Management

- Lazard Asset Management provides excellent summary of reform Temer

- EME turbulence and political risks in Mexico and Brasil - Monica de Bolle 2018

- Brazil elections - can a nerw president save the economy Aljazeera

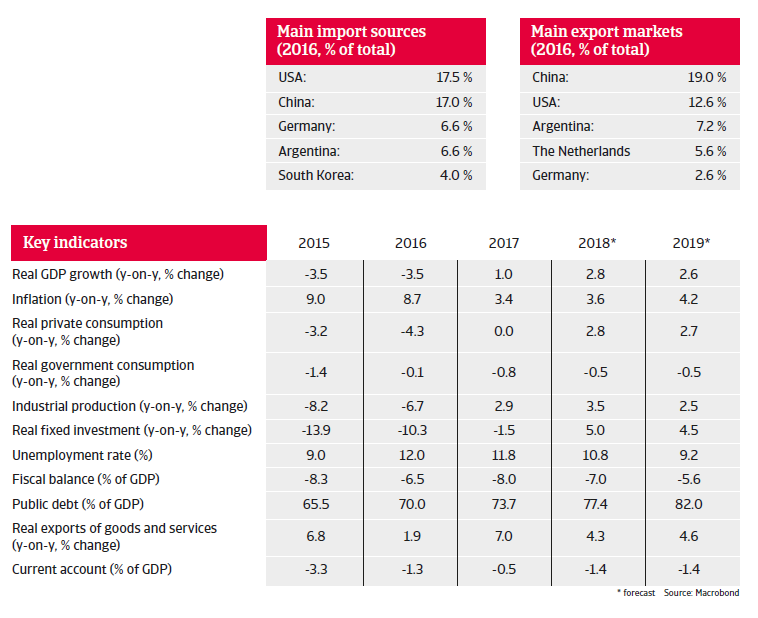

- Country report for Brasil 2018 from Atradius - includes graphic below